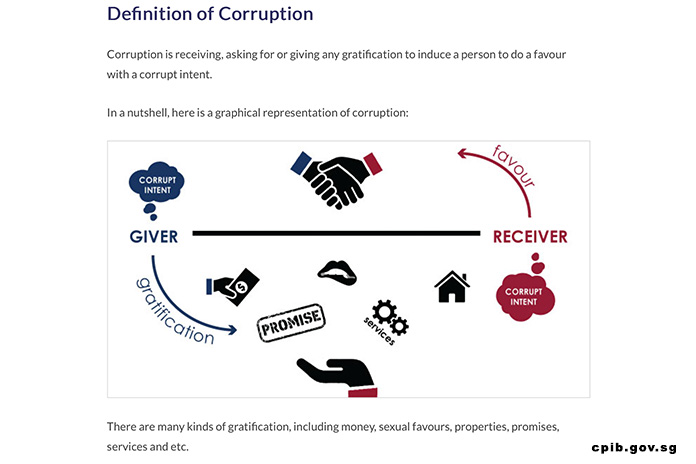

RECENT cases of corruption involving corporations and members of the private and public sectors seem to have dulled the lustre of Singapore’s reputation for running a clean business environment.

The government, quick to buff its image, has stepped up measures to contain and control the situation.

On the Corrupt Practices Investigation Bureau (CPIB) website, the latest Corruption Statistics are from 2020, where Singapore is ranked #3 among 180 countries according to the Transparency International Corruption Perceptions Index. The 2022 index ranks Singapore at #5.

With an 87% clearance rate and 97% conviction rate, not many will escape the clutches of the system that doesn’t like anyone to evade paying their dues.

The CPIB is the world’s oldest anti-corruption agency, established in 1952. The world has changed significantly since then, offering opportunities for corruption to take place in the physical and virtual realms.

How do organisations address and eliminate corruption in their system? With remote working and offices in many part of the world, there are several aspects of the business that need to be monitored on a constant basis.

STORM-ASIA talks to business owners and accountants about the best practices to institute in organisations to keep out corruption.

ALSO READ: Turning Old Lights Into New Art

Hard Landing

The importance of having a strong internal audit function can be seen in the well-publicised fraudulent case by Teo Cheng Kiat of Singapore Airlines. He was in charge of processing SIA cabin crew allowances, and by making false claims and channeling the payments to his own bank account he managed to syphon off almost $35 million over a period of 13 years.

According to the CAD (Commercial Affairs Department of the Singapore Police Force) files made public in the media on 29 March 2004, his superiors had failed to carry out proper checks and there were loopholes in the system. He was a trusted employee and thus was not suspected of possible wrongdoing.

It was an ad hoc review by the internal audit department of data on the daily allowance payment which uncovered possible fraud. On three individual bank accounts there were 10 payments each. There should not be more than one payment of allowance to any crew member on a particular day. Teo was sentenced to 24 years’ imprisonment.

This case also illustrates the importance of executing proper checks even on trusted employees. Checks and balances are not to cast aspersion on any individual but are designed to detect errors early and the possible detection of frauds.

Rules To Abide By

The core values of a business must emphasise integrity and honesty. There must also be in place an effective whistle-blowing system where whistle-blowers know they are protected and are encouraged to provide any evidence of wrongdoing.

The consequence of being found guilty of corruption must be severe enough as a deterrence.

There must be in place a system of good internal controls with effective checks and balances. Individuals with assigned responsibility must be held accountable.

A classic example is the case when there are three levels of approval as control, say for procurement and each of the three assigned controllers assumes that the other two will be doing a thorough check and thus pays little attention to his own check. As a result, no thorough check gets done and the control breaks down.

The larger the organisation, the greater the need for a strong internal audit function. With millions of transactions each year, the only meaningful way of implementing internal checks is to adopt analytics to look for patterns of discrepancies. The cost of investing in an effective internal checking system will be more than offset by reducing the risk of a major fraud which could cost the organisation dearly, not just in terms of financial loss but reputational damage, which takes years to repair and regain the trust of partners, customers, and other stakeholders.

The organisation must put in place a robust Enterprise Risk Management system and always be mindful of what could go wrong. All organisation must live with risks in a rapidly changing economic order and it becomes necessary to have effective mitigating process to manage the risks which an organisation have to live with.

ALSO READ: Rolex Plays Its Hand In The Watch Industry

Laundry List

As a self-storage business invested in by US-based investors, StorHub primarily adopts the definition laid out in the US Foreign Corrupt Practices Act,

“It is unlawful for a … person or company to offer, pay, or promise to pay money or anything of value to any foreign official [we add company and individual] for the purpose of obtaining or retaining business.” However, because of the multiple places StorHub operates in, all of the specific legislation we have to follow are:

(a) the US Foreign Corrupt Practices Act of 1977 and the rules and regulations issued thereunder;

(b) the UK Bribery Act of 2010;

(c) the Prevention of Corruption Act (Chapter 241) of Singapore;

(d) the Prevention of Bribery Ordinance (Chapter 201) of Hong Kong;

(e) provisions in the Criminal Law of the PRC and the Anti-Unfair Competition Law of the PRC.

This is obviously quite painful to keep track of….

Housekeeping

We need to have a combination of a formal structure to dissuade and detect corrupt activity (trust but validate) along with an informal culture that encourages people to not think about or not feel motivated to engage in corrupt activity that will harm a culture and a company that has meaning for them.

- Every year, we conduct anti-corruption training programmes, run by an external party such as Ernst & Young.

- When we hire new staff, we ask them to sign a document to state that they will not engage in a variety of corrupt activities which we list out.

- Our Standard Operating Procedures are as well designed as we can make them to reduce the opportunity for leakage.

- We pay for top-tier auditors to audit every one of our companies.

- We have a whistleblower hotline and strongly encourage staff to use this to report suspicious activity, even if they are not certain.

- On top of these, we aim to pay in the top segment of our industry (real estate, not just self-storage) and manage our staff well enough that they do not feel the need to enrich themselves further.

Red Flags To Note

The continued use of the same suppliers is often a common warning sign. We continually re-quote and re-tender key supply contracts.

Vendors or suppliers who are unwilling to provide sufficient detail on sourcing and costing would also raise a red flag.

We benchmark against previous, similar purchases and audit review purchasing documentation to ensure supply chains are free from corruption and unethical practices.

ALSO READ: Find Your Why In Life

Building Up Rather Than Breaking Down

Corruption and corrupt practices have been present throughout human history, fuelled by greed and temptation.

Although every organisation is different, the definition of corruption remains the same. Achieving a large degree of success in anti-corruption initiatives involves partnering with NGOs or government agencies, implementing strict internal controls, conducting corruption risk assessments, and engaging in collective action with other businesses.

While it’s challenging to completely eradicate them, organisations can mitigate their incidence by fostering a culture of accountability and prioritising the interests of the company over personal gain.

Effective measures to combat corruption involve building trust and integrity as pillars of a strong business foundation. Transparency, accountability, and ethical behaviour are crucial principles for organisations, along with implementing robust internal controls and adhering to laws and regulations.

To prevent corrupt practices, organisations should establish codes of conduct, anti-corruption policies, and whistleblower mechanisms. Performing due diligence on business associates and suppliers is also essential to ensure ethical supply chains free from corruption and unethical practices.

While eliminating corruption entirely may not be attainable, dedicated efforts can significantly reduce its impact and promote ethical business practices.

Nothing Is Foolproof

It is never an easy decision to make to walk away from a business opportunity, especially when there are revenue goals to meet, but walk away I did on many occasions, doing business in the Asia-Pacific.

When I was working for Compaq (the largest supplier of PCs in the 1990s), I was required, as the CEO and legal representative, to confirm annually that I did not engage in any bribery or corruption.

Although a company can have a policy against bribery and corruption, and in many cases compliant with a country’s laws, many past cases of violations have proven that it is not sufficient and foolproof as a deterrent.

What is ultimately required is the incumbent’s discipline and gumption to walk away from the temptation, especially when it involves losing a potentially lucrative business deal.

In all my 50 years of working up to the present, I am guided by the 3Hs — Honour, Honesty and Humility. This was instilled in me by my grandfather and later on by my dad.

I was taught that it is not good enough to win a business honourably, but it has also to be won honestly.

To bribe or be corrupt is dishonourable and dishonest. For me, my reputation and that of the company that I worked for in relation to bribery and corruption are worth more than the business that I have foregone.

It has been proven time and again, that this will pay dividends in the future. As an example, Compaq grew the PC business from under US$30m to US$1B, from 1988 to 1995, in Asia-Pacific without a single cent being paid as a bribe. It shows that while there may be a temporary glitch in the business when a deal is lost, a company is better off in the longer term, as it arms the company not to have to depend on bribery or corruption to grow the business.

Nice Article